Allen Hu

Assistant Professor of Finance

UBC Sauder School of Business

Email: allen.hu@sauder.ubc.ca

Research Interests:

Big Data and AI in Finance

Information in Financial Markets

Entrepreneurial Finance and Behavioral Finance

Publications

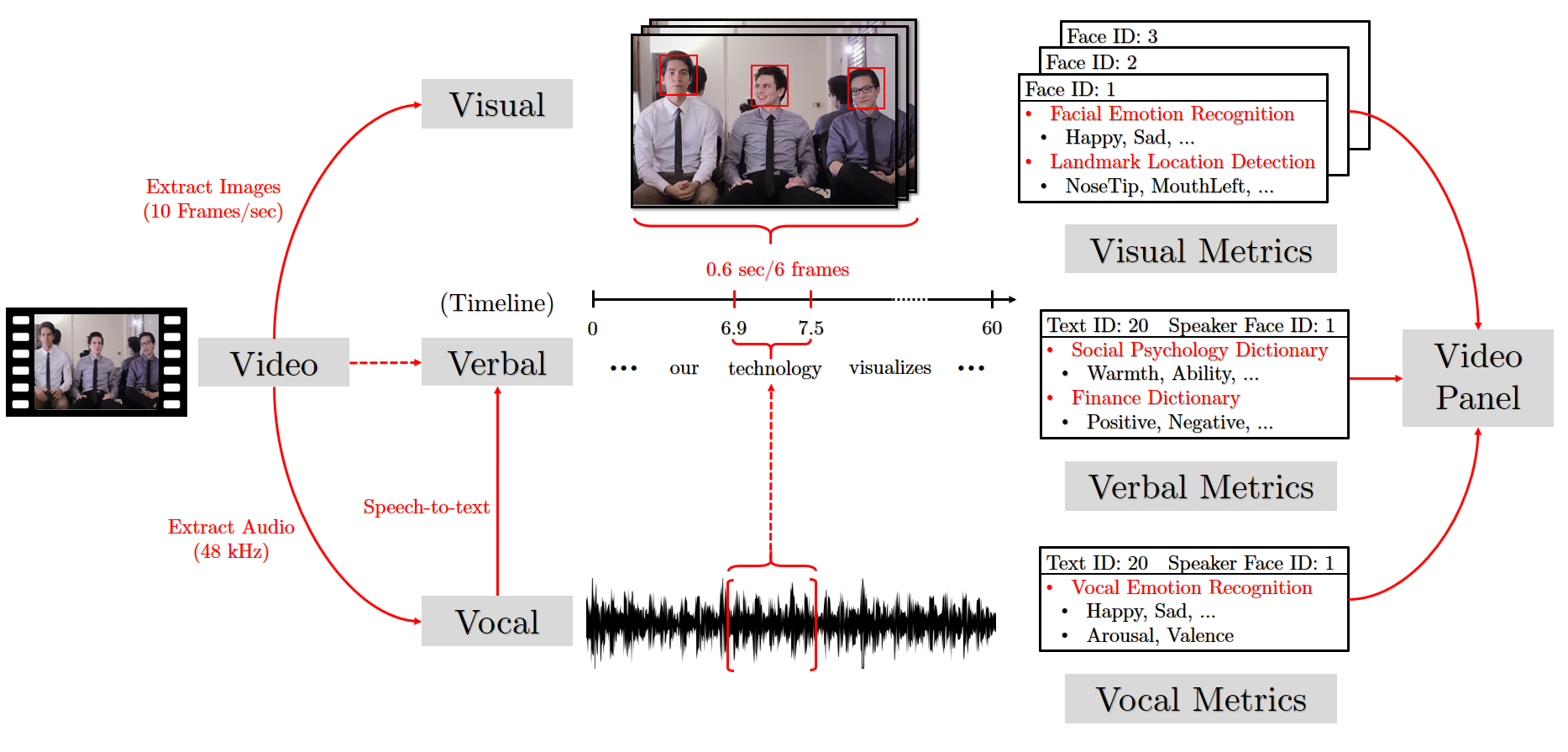

Persuading Investors: A Video-Based Study

Asset Complexity and the Return Gap

Working Papers

How Do Banks Compete? Evidence from Advertising Videos

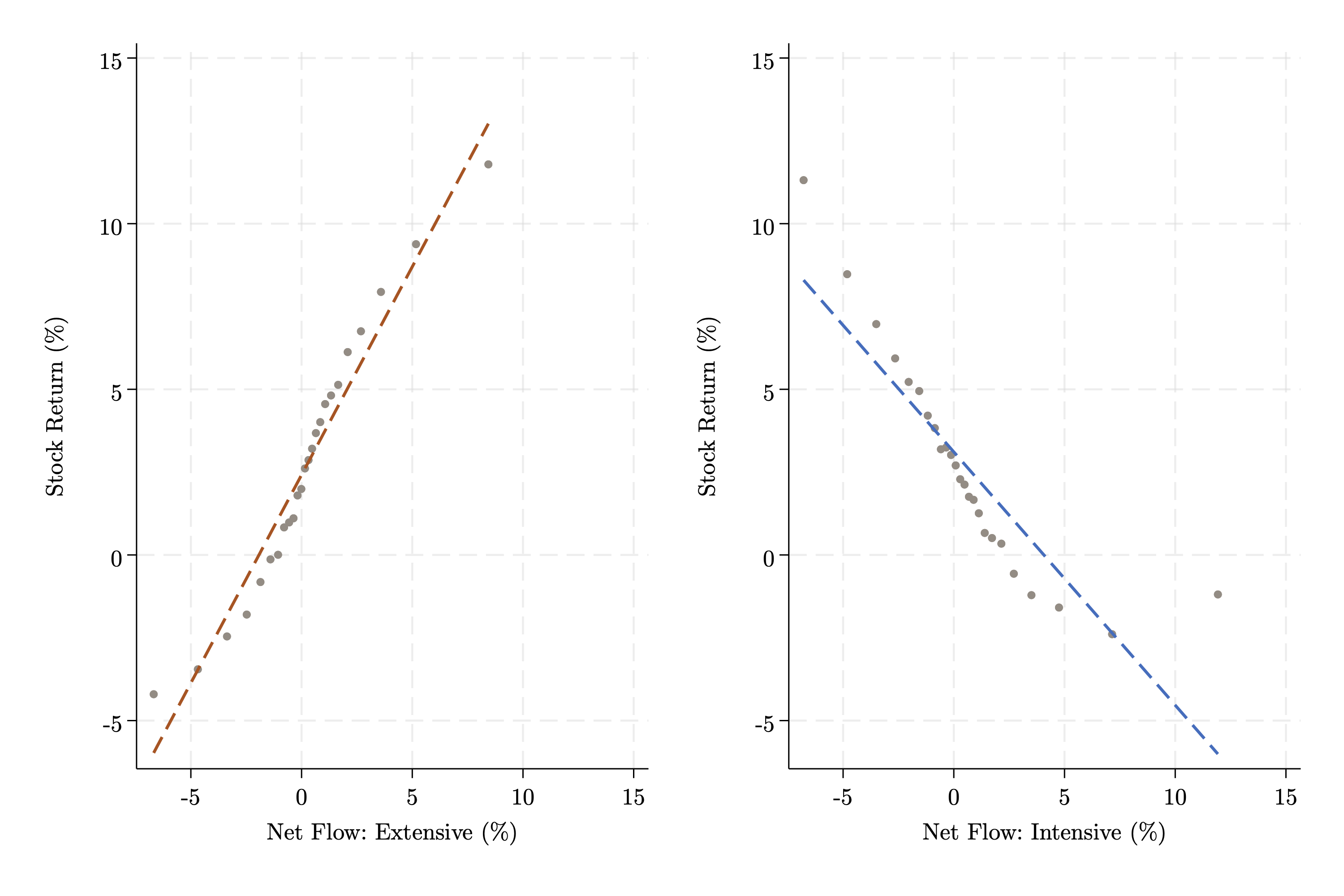

Inelastic Demand at the Extensive and Intensive Margins

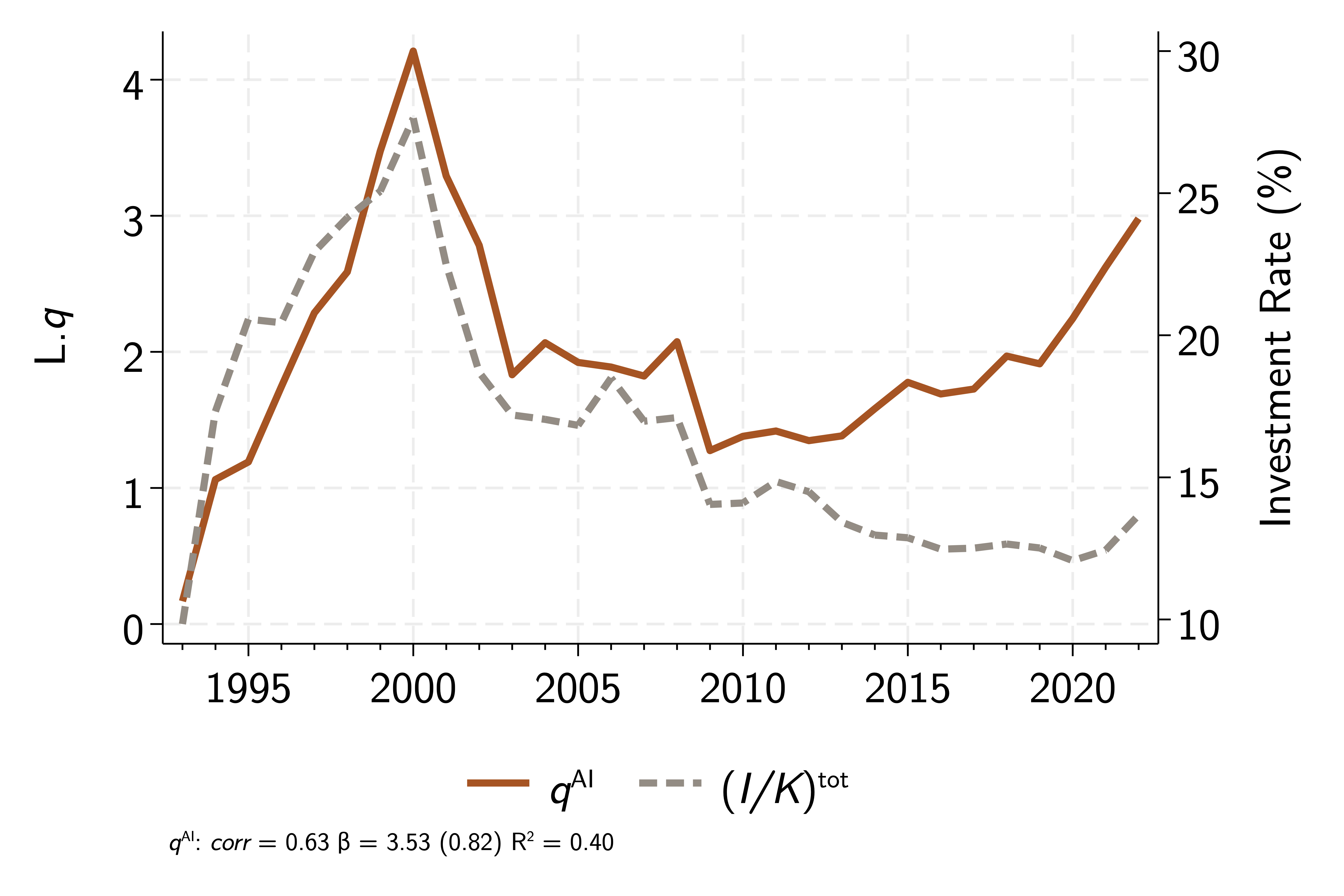

Putting Marginal Back in Tobin's q

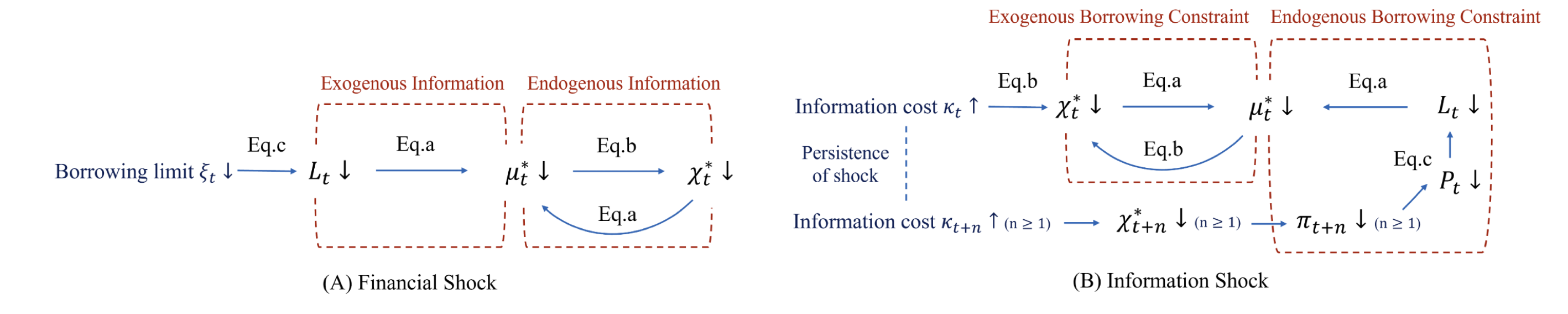

Information Acquisition and the Finance-Uncertainty Trap

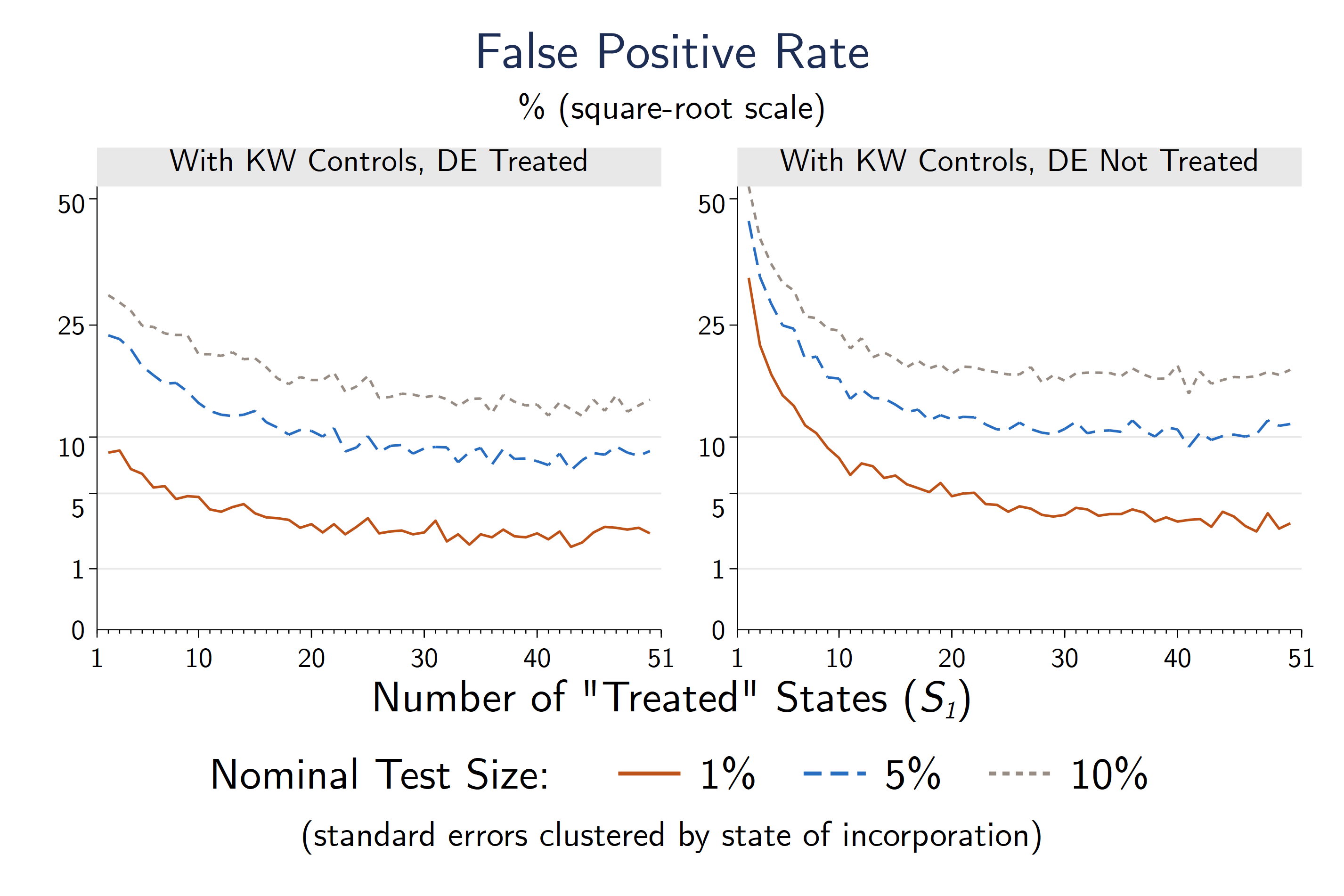

Inference with Cluster Imbalance: The Case of State Corporate Laws

Reject & Resubmit at Review of Financial Studies

Work in Progress

Contact

- Email:

- allen.hu@sauder.ubc.ca

- Phone:

- +1 (604) 827-1609

- Office:

- 862 Henry Angus Building

- Address:

- 2053 Main Mall, Vancouver, BC, Canada V6T 1Z2

About

Allen Hu is an Assistant Professor of Finance at Sauder School of Business, the University of British Columbia. Prior to joining UBC, he obtained his Ph.D. in Financial Economics from Yale School of Management in 2024 and his B.E. in Industrial Engineering from Tsinghua University in 2017. His primary research areas are big data and AI in finance, information in financial markets, entrepreneurial finance, and behavioral finance.

Links

Curriculum Vitae (PDF)

UBC Sauder Faculty Page

Google Scholar

SSRN

LinkedIn